Kyoki (Insanity)

Pondering the state of the global economy can elicit manic‐depressive‐obsessive‐compulsive emotions. The volatility of global markets – equities, bonds, commodities, currencies, etc. – are challenging enough without consideration of Brexit, the U.S. Presidential election, radical Islamic terrorism and so on. Yet no discussion of economic and market environments is complete without giving hefty consideration to what may be a major shift in the way economic policy is conducted in Japan.

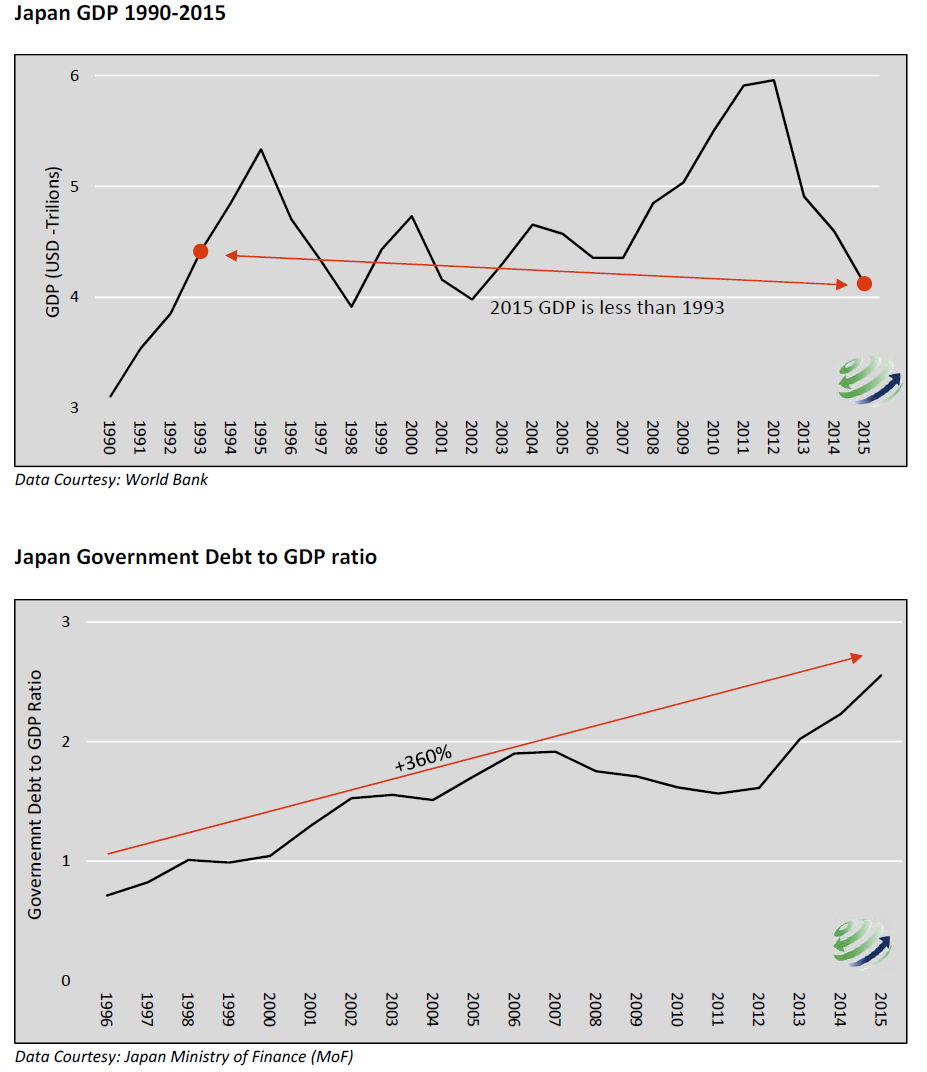

The Japanese economy has been the poster child for economic malaise and bad fortune for so long that even the most radical policy responses no longer garner much attention. In fact, recent policy actions intended to weaken the Yen have resulted in significant appreciation of the yen against the currencies of Japan’s major trade partners, further crippling economic activity. The frustration of an appreciating currency coupled with deflation and zero economic growth has produced signs that what Japan has in store for the world falls squarely in to the category of“you ain’t seen nothin’ yet.” Assuming new fiscal and monetary policies will be similar to those enacted in the past is a big risk that should be contemplated by investors.

The Last 25 Years

The Japanese economy has been fighting weak growth and deflationary forces for over 25 years. Japan’s equity market and real estate bubbles burst in the first week of 1990, presaging deflation and stagnant economic growth ever since. Despite countless monetary and fiscal efforts to combat these economic ailments, nothing seems to work.

Any economist worth his salt has multiple reasons for the depth and breadth of these issues but very few get to the heart of the problem. The typical analysis suggests that weak growth in Japan is primarily being caused by weak demand. Over the last 25 years, insufficient demand, or a lack of consumption, has been addressed by increasingly incentivizing the population and the government to consume more by taking on additional debt. That incentive is produced via lower interest rates. If demand really is the problem, however, then some version of these policies should have worked, but to date they have not.

The value of listed Japanese companies' future obligations to retiring workers reached a record 91.21 trillion yen ($860 billion) at the end of fiscal 2015, with the unfunded chunk growing to nearly 26 trillion yen amid depressed interest rates.

As Venezuela’s crisis swells, its gold reserves are shrinking. The holdings fell again in May, sliding to 6.24 million ounces from 6.63 million ounces in April to post a fourth consecutive drop, according to data from the International Monetary Fund website. Over the past year, the country’s hoard has shrunk 36 percent, and since February 2015 it’s nearly halved.

Overall classified loan exposure, which includes debts that are unrecoverable as well as those unlikely to be repaid, rose to a seven-year high of 0.92 percent by March, according to Monetary Authority of Singapore data.

Shell misses expectations with 70 percent earnings plunge